All Categories

Featured

Table of Contents

[/image][=video]

[/video]

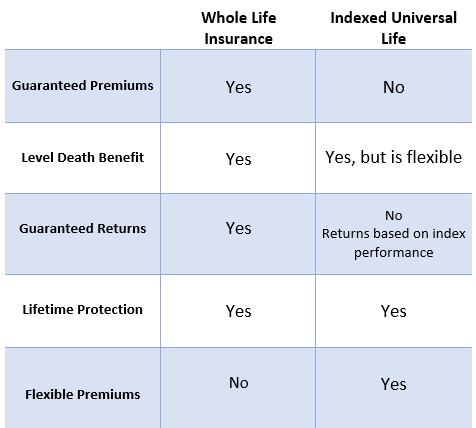

You can underpay or miss premiums, plus you may be able to readjust your fatality benefit.

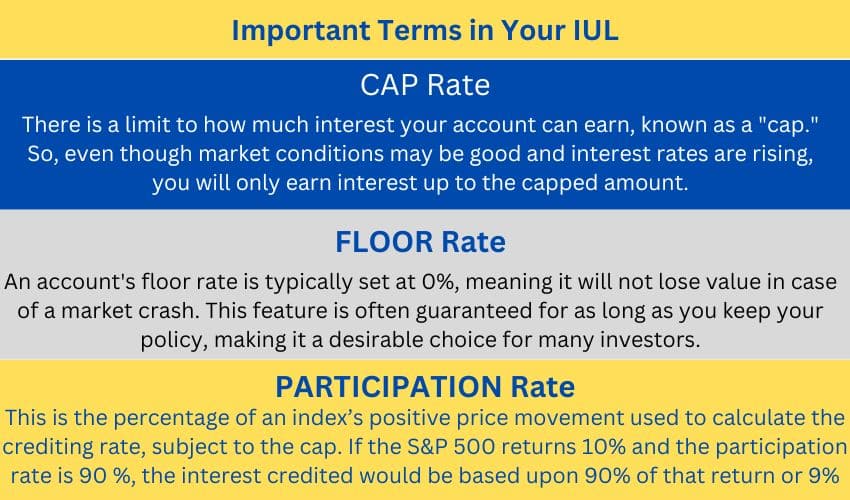

Flexible costs, and a fatality benefit that may likewise be adaptable. Money value, in addition to potential development of that value with an equity index account. A choice to assign component of the money worth to a set rate of interest choice. Minimum rate of interest guarantees ("floorings"), yet there may also be a cap on gains, typically around 8%-12%. Collected money value can be utilized to reduced or possibly cover costs without subtracting from your survivor benefit.

Equity Indexed Universal Life Insurance Questions

Insurance policy holders can choose the portion alloted to the taken care of and indexed accounts. The value of the selected index is videotaped at the beginning of the month and compared to the worth at the end of the month. If the index boosts throughout the month, rate of interest is contributed to the cash money worth.

The 6% is increased by the cash value. The resulting passion is included to the cash worth. Some policies calculate the index acquires as the sum of the modifications through, while various other plans take a standard of the everyday gains for a month. No rate of interest is attributed to the cash account if the index goes down as opposed to up.

Iul Life

The rate is set by the insurer and can be anywhere from 25% to even more than 100%. (The insurance provider can likewise transform the take part rate over the life time of the plan.) As an example, if the gain is 6%, the participation price is 50%, and the existing cash money worth total amount is $10,000, $300 is added to the cash worth (6% x 50% x $10,000 = $300).

There are a number of pros and cons to think about before buying an IUL policy.: Similar to common universal life insurance policy, the insurance holder can boost their premiums or lower them in times of hardship.: Quantities attributed to the money worth grow tax-deferred. The cash worth can pay the insurance policy premiums, enabling the insurance policy holder to lower or quit making out-of-pocket premium settlements.

Many IUL plans have a later maturation date than other types of global life plans, with some ending when the insured reaches age 121 or more. If the insured is still to life back then, plans pay the death benefit (yet not typically the cash value) and the proceeds might be taxed.

Best Indexed Universal Life Insurance Policies

: Smaller policy face worths don't offer much benefit over regular UL insurance policies.: If the index goes down, no interest is attributed to the money worth.

With IUL, the objective is to make money from higher activities in the index.: Because the insurance policy business just acquires choices in an index, you're not directly invested in stocks, so you do not profit when business pay returns to shareholders.: Insurers cost costs for managing your money, which can drain pipes money value.

For most individuals, no, IUL isn't better than a 401(k) in regards to saving for retired life. Most IULs are best for high-net-worth individuals seeking methods to minimize their taxable income or those that have maxed out their other retired life options. For everybody else, a 401(k) is a much better financial investment automobile since it doesn't carry the high costs and premiums of an IUL, plus there is no cap on the amount you may earn (unlike with an IUL policy).

While you may not shed any kind of money in the account if the index goes down, you will not earn interest. The high cost of premiums and costs makes IULs pricey and substantially less inexpensive than term life.

Indexed global life (IUL) insurance offers money value plus a fatality advantage. The cash in the cash money worth account can make rate of interest via tracking an equity index, and with some commonly alloted to a fixed-rate account. Indexed universal life plans cap exactly how much cash you can accumulate (usually at less than 100%) and they are based on a perhaps unstable equity index.

Indexed Universal Life Insurance

A 401(k) is a much better alternative for that function since it doesn't lug the high costs and costs of an IUL plan, plus there is no cap on the amount you might earn when invested. Many IUL policies are best for high-net-worth people seeking to decrease their taxable earnings. Investopedia does not give tax obligation, financial investment, or financial services and guidance.

FOR FINANCIAL PROFESSIONALS We've created to give you with the most effective online experience. Your existing internet browser could limit that experience. You might be using an old browser that's in need of support, or setups within your web browser that are not compatible with our website. Please conserve yourself some stress, and update your internet browser in order to watch our website.

Already making use of an upgraded internet browser and still having trouble? Please provide us a telephone call at for further support. Your present internet browser: Spotting ...

Iul Vs Term Life

When your selected index gains value, so as well does your plan's cash money value. Your IUL cash money worth will additionally have a minimum rate of interest that it will constantly make, despite market performance. Your IUL might additionally have a rate of interest cap. An IUL policy works similarly as a conventional global life plan, with the exemption of just how its money value earns interest.

Insurance Iul

If you're thinking about getting an indexed global life plan, very first talk to an economic advisor who can discuss the nuances and offer you an exact image of the actual capacity of an IUL policy. See to it you comprehend exactly how the insurance provider will certainly calculate your interest rate, earnings cap, and fees that may be examined.

Part of your costs covers the plan cost, while the remainder enters into the cash value account, which can expand based upon market performance. While IULs may appear attractive, they normally feature high costs and inflexible terms and are entirely unsuitable for lots of financiers. They can create passion yet also have the possible to lose money.

Here are some variables that you need to consider when identifying whether a IUL plan was appropriate for you:: IULs are complex monetary products. Make certain your broker fully discussed just how they work, including the prices, financial investment threats, and charge structures. There are more affordable options offered if a survivor benefit is being looked for by a financier.

Best Iul Provider

These can substantially lower your returns. If your Broker fell short to provide a thorough description of the costs for the plan this can be a warning. Understand surrender charges if you determine to cancel the plan early.: The financial investment component of a IUL is subject to market fluctuations and have a cap on returns (meaning that the insurer receives the advantage of stellar market performance and the investor's gains are capped).

: Ensure you were outlined and have the ability to pay enough costs to keep the policy in force. Underfunding can bring about plan gaps and loss of coverage. If your Broker falls short to discuss that costs settlements are required, this can be a warning. It is crucial to completely study and understand the terms, charges, and possible threats of an IUL plan.

Traditional development investments can typically be coupled with much less costly insurance coverage options if a death advantage is very important to a financier. IULs are excluded from government guideline under the Dodd-Frank Act, indicating they are not looked after by the U.S. Stocks and Exchange Commission (SEC) like supplies and choices. Insurance policy agents marketing IULs are just called for to be licensed by the state, not to go through the very same rigorous training as financiers.

{kind=link}

Latest Posts

Disadvantages Of Indexed Universal Life Insurance

Iul Life Insurance Pros And Cons

Indexed Universal Life Insurance Companies